Oath-takers and tax-payers in Georgian Stokenham

By Paul Luscombe

Documentary sources

A full description of the oath rolls is available on this website in Simon Dixon's introduction, including the scope of the legislation ('The legal requirements') and how the process was organised ('The administration of the oaths').2 As he indicates, the Oath Act of 17233 does not define exactly who was expected to take the oath, though local directives from the County Quarter Sessions refer - but not exclusively - to freeholders, copyholders and other owners of real estate ('the Exeter press and the oaths'). Nearly all of those from Stokenham who took the oath made the journey to Kingsbridge on 28 August 1723 (95 names), 29 August (25 names), 4 November (27 names) or 5 November (10 names) of that year. A further Stokenham signatory went to Moreleigh on 26 August, while another 10 had already sworn in 1714 or 1715, mainly at Moreleigh or Exeter (listed in the 'pre-1723 Indexes').

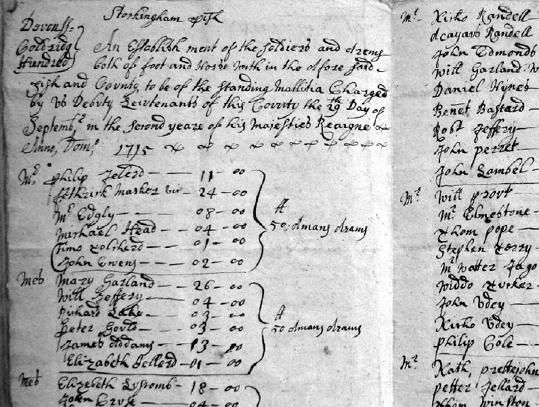

The militia assessments are quite different. They were valuations for a tax, raised under the Militia Acts of 1662 and 1663, and paid by property owners according to a somewhat complicated scale. In summary, those with property valued at £50 per annum paid for a foot soldier; those holding property at lower values were grouped so that the aggregate values amounted to £50 per annum; and landowners with larger estates had to find or contribute towards the cost of a horse in the cavalry. These records have not survived to the same extent as the much more common muster rolls which had the function of listing the names of soldiers who served in the militia, rather than the taxpayers who paid for its upkeep.4 The assessments for Herefordshire have been transcribed and published by the Royal Historical Society with a useful and detailed introduction, while the political and military background is supplied by J. R. Western.5 A transcript of most of the South Devon assessments is available in the search room at the DHC. It includes "An Account of the Men to be raised towards the Militia" for Coleridge and Stanborough Hundreds, showing that Stokenham's quota was 17 men, the same as those for Harberton and Diptford parishes, but less than the numbers to be raised in Malborough (24) and West Alvington (21).6 The size of the militia was intended to be roughly proportionate to the value of property in each county and in each parish. Figure 2 is a facsimile of part

Figure 2: Stokenham militia assessment (part) for men and "Arams" (arms). DHC Z1/43/1 (reproduced by permission).

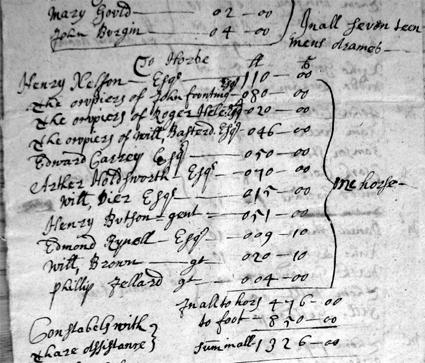

of the Stokenham assessment showing the property owners arranged in groups with land valued at £50 per annum in aggregate The valuations range from £1 to £35 per annum for foot-soldiers and up to £110 per annum for payments to support the cavalry (figure 3). One of their uses (which is not pursued here) might be to show the distribution of wealth within a parish and between parishes.

Figure 3: Stokenham militia assessment (part) for cavalry. DHC Z1/43/1 (reproduced by permission).

The third documentary source is the parish register for Stokenham. It has been tolerably well kept for most of the latter part of the seventeenth and the first part of the eighteenth centuries. Between 1660 and 1740 baptisms and burials are low in each of about five years,7 with gaps in the marriage register in 1679-80, 1710, 1725 and 1736. The register is remarkable in one respect: for nearly 64 years, from his induction, aged 29 in 1674 until his burial in 1738, one incumbent, Frederick Marker, was responsible for the cure of souls in Stokenham and for the baptisms, marriages and burials of his (conforming) parishioners. His usually neat, if sometimes cramped, italic hand records their rites of passage from 1688 to the end of the 1720s when the writing begins to deteriorate, perhaps through failing sight and arthritis, until in 1734 it gives way to a different hand.

Continue to next section Return to previous

- Simon Dixon (ed.), Devon and Exeter Oath Rolls, 1723, Friends of Devon's Archives [www.foda.org.uk/oaths, accessed May 2007]. [Back]

- 9 Geo I, cap. 24. [Back]

- For the muster rolls, see Jeremy Gibson & Alan Dell, Tudor and Stuart Muster Rolls (Federation of Family History Societies, 1991); Jeremy Gibson & Mervyn Medlycott, Militia Lists and Musters 1757 - 1876 (Federation of Family History Societies, 2000). A search on the Access to Archives [http://www.a2a.org.uk, accessed 15 June 2007] website seems to indicate that few militia assessments have survived. [Back]

- M. A. Faraday, Herefordshire Militia Assessments of 1663, Royal Historical Society, Camden 4th Series, volume 10 (London, 1972); J. R. Western, The English militia in the eighteenth century: the story of a political issue, 1660-1802, (London, 1965). [Back]

- DHC Z1/43/1. [Back]

- For baptisms, 1688, 1705, 1707, 1726 and 1736; for burials, 1668, 1711�12 (gap in register), 1719-20 and 1737. [Back]